There are many financial strategies to consider throughout the year with your financial advisor and tax accountant. By the end of the year, we know more about next year’s numbers, and we not only strategize for this year, but also the year to come. Making informed choices every year and small yet important adjustments will lead to greater wealth and less taxes paid in your lifetime and beyond.

Key Strategy Areas

- Maximize your tax-deferred savings — During your working years, retirement contributions are generally your strongest tax-saving opportunity. Take advantage of the increased limits in these accounts. If you’re approaching a key age milestone (50+ or, in some cases, 60–63) and fall within certain income thresholds, you may also qualify for additional “catch-up” or enhanced “super catch-up” contribution amounts.

- Consider partial Roth Conversions — Converting a portion of traditional IRA or 401(k) assets in lower-income years can secure tax-free growth and help manage future RMDs.

- Review charitable-giving timing and vehicles — A well-timed gift can provide tax relief and accomplish philanthropic goals. With tax law changes taking effect in 2026, making (and even accelerating) charitable gifts in 2025 may offer greater benefits.

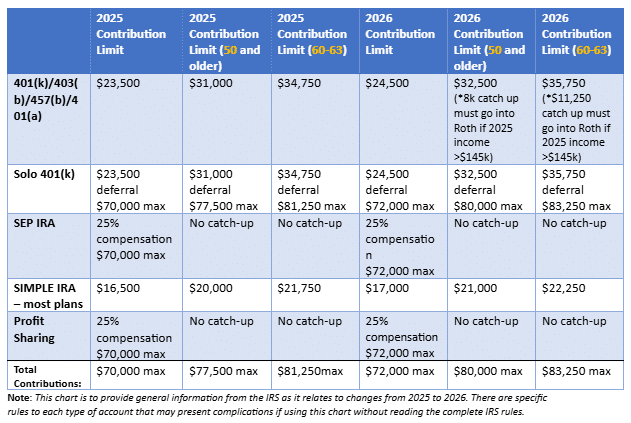

Tax Deferred Contribution Limits for 2025 and 2026

Contributing to a tax-deferred retirement account can reduce your taxable income. Contribution/deferral limits for 2026 have been announced by the IRS and can be seen in the chart below alongside 2025 limits. Take advantage of 2025 limits before year end and set up accounts to take advantage of 2026 deferral limits in the new year.

Does your employer match your contributions? Don’t leave money on the table. Make sure to contribute at least the amount that will maximize your employer’s contribution to your retirement account. If your employer doesn’t offer an employer sponsored plan, your traditional IRA contributions may be tax-deductible. The deduction may be limited if you or your spouse is covered by a retirement plan at work and your income exceeds certain levels.

A new rule starting in 2026 impacts high earners 50 and above who make catch up contributions to employer sponsored plans. Those making more than $145,000 in the prior year will have to put their catch-up dollars in a Roth 401(k)—which means you won’t get a tax deduction, but their qualified withdrawals in retirement will be tax free. The catch-up amount could be included in what employers will match.

The IRS announced increases in contribution limits to IRAs as well (see below). There are no longer age limits on contributing to a traditional or Roth IRA. However, there are income limits that need to be met to contribute pre-tax money to a traditional IRA and after-tax money to a Roth IRA.

Health Savings Account contribution limits will increase in 2026 for individuals and families. The catch-up amount for people aged 55 and older stays at $1,000 for individuals and families. Learn to make the most of a Health Savings account by reading our blog here.

There are various deadlines for contributions to the above accounts ranging from December 31st,2025 to March 15th, 2026 to April 15th, 2026 to October 15th, 2026 (if the business has a tax-filing extension) to be coded as a 2025 contribution. Consult your plan administrator, your tax accountant, or the IRS site for accurate deadlines.

Roth Conversions

A Roth IRA conversion allows the transfer of some or all your retirement savings from a Traditional IRA, Rollover IRA, SEP-IRA, SIMPLE IRA, or 401(k) into a Roth IRA. There are no age limits to completing a Roth Conversion and also no income restrictions, as there are when contributing to a Roth IRA.

A conversion to a Roth IRA results in taxation of any untaxed amounts in the traditional IRA, like a normal IRA distribution. The assets, now in a Roth IRA, grow tax-free. Withdrawals after the age of 59.5 and the earnings after 5 years are also tax-free. The 5-year duration is calculated from the 1st day of the year you contribute/convert to your Roth IRA. Doing a conversion in December takes almost a year off the 5-year requirement.

Another reason the end of the year is a great time to consider doing a partial Roth Conversion is because you may have a better understanding of your annual income and hence where you fall in your tax bracket. Your tax accountant can help you calculate the amount to convert to stay within your tax bracket.

Down markets can present opportunities for Roth Conversions. In a down market, converting stocks that have been hit hard and that are expected to rebound is a strategy to consider. Simply put, you’ll pay tax on lower values now and benefit from potential tax-free gains in the future. A trusted financial advisor can help you identify these stocks and process the conversion. Converted amounts are taxable in the same year. It is optimal when there is available cash outside these accounts to cover the taxes.

Charitable Giving Deductions for 2025 and 2026

How do you like to give? Here are a few giving strategies that have tax-saving advantages, making your contribution to your favorite charity doubly rewarding.

Donations to charities, as defined by the IRS, are tax-deductible and can lower your taxable income in the year the donation is made. It is important to ensure that any charitable giving meets IRS substantiation rules when itemizing your contributions as deductions. The IRS has announced that the standard deductions for taxpayers will go up in 2026. See the chart below.

Consider “batching” your donations every few years to maximize using the standard deduction in the years when you don’t itemize. This can be done in conjunction with consolidating non-emergency visits to doctors and dentists to help you surpass the AGI threshold required for deductibility, maximizing the tax benefit.

“Give away the gain” – Gifting shares of stock that have appreciated significantly from the time you bought them to a qualified organization, can avoid incurring tax on capital gains (if the security were to be sold and the gain realized).

Gifting highly appreciated assets from taxable accounts to a Donor Advised Fund (DAF), is also a way to secure a charitable deduction in 2025 and avoid capital gains. Once the assets are in a DAF, you can watch them grow tax-free and give them to qualified charities in future years. The year in which you transfer assets to a DAF is the year you can lower your tax burden. Therefore, consider this strategy in years with high income.

Another tax-saving way to give is through Qualified Charitable Distributions (QCD). Individuals 70.5 years old and older can perform charitable IRA rollovers and directly transfer up to a total combined of $111,000 (up from $108,000 in 2025) from their IRA(s) to qualified charities. Taxes are neither withheld nor incurred for QCD distributions, and the amount can be used to offset Required Minimum Distributions (RMD), reducing Adjusted Gross Income (AGI). For those who are RMD age, have plans to give to charity, and don’t need to take the entire distribution for income; this is a highly effective way to lower taxes!

Tax Law Changes – starting in 2026, charitable deductions will be reduced by a new 0.5% AGI floor, limiting the portion of your giving that can be written off. For example, with a $200,000 AGI, the first $1,000 you donate will not be deductible. In addition, individuals currently in the 37% bracket will see all itemized deductions capped at an effective rate of 35%. That means a $10,000 charitable gift would generate $3,500 in tax savings in 2026, compared with $3,700 in 2025 — making gifts completed in 2025 more beneficial. As a result, making planned gifts now or even accelerating future-year charitable contributions into 2025 may provide a stronger tax advantage before these changes take effect. These new tax laws make charitable giving through Qualified Charitable Distributions (QCDs) even more advantageous as they skirt around the .5% floor and 37% bracket cap.

The deadline for charitable giving is Dec 31st 2025, to claim a tax deduction for 2025. December 1st is the recommended latest date to initiate gifts of qualified, appreciated stock or wire transfers and IRA charitable rollovers/QCDs to ensure they are received by the end of the year.

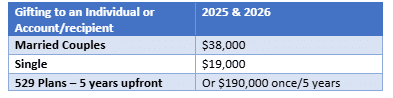

Gifting Limits for 2025 and 2026

The annual gifting limit will remain the same next year. Individuals may give up to $19,000 per recipient without using any of their lifetime estate- and gift-tax exemption. For married couples, this amount is doubled. For example, you could give $19,000 to an adult child to help with a home down payment, and your spouse could gift another $19,000, thus allowing a couple to transfer $38,000 in one year without reducing their lifetime exemption. A couple can also elect to use five years of exclusions upfront, enabling them to gift $190,000 at once. Just make sure your CPA is aware, since the five-year gifting election requires filing Form 709 for documentation purposes.

To fund the specific goal of contributing to a young child’s future educational expenses, you can make contributions to a 529 plan as a gift. When markets are down and children are young, it could be the ideal time to increase contributions to 529 accounts.

In 2026, the federal estate and gift tax exemption will be $15 million per person (or $30 million for married couples). If you are near or above these thresholds, making annual gifts of up to $19,000 per recipient is an effective way to gradually reduce your taxable estate.

Tax Loss Harvesting

Although we do not recommend selling good investments for tax purposes only, tax loss harvesting can be a useful tool at the end of the year to avoid some or all capital gains tax within a taxable account.

Selling securities at a loss can offset realized gains from other sales. In addition, if your capital losses exceed your capital gains, the amount of the excess loss that you can claim to lower your income is the lesser of $3,000 ($1,500 if married filing separately) or your total net loss. If your net capital loss is more than this limit, you can carry the loss forward to later years.

It is important to be aware of the wash sales rules. The IRS won’t let you claim the loss if you sell the stock and then buy a “substantially similar” stock in any of your or your spouses’ accounts within 30 days. After 30 days, you are allowed to buy the same or similar stock back and still account for the loss.

Tax Loss Harvesting can be especially useful for taxable accounts in periods of market volatility. A trusted financial advisor can help you identify the securities to sell to realize a loss, identify the securities to reinvest the proceeds in, and avoid wash sales in the process.

Seek Advice

Contribution limits and tax laws change frequently, and your life and financial situation might change just as often. To sort through these end-of-year strategies, find a trusted financial advisor who will work closely with your tax accountant to determine what important adjustments can be made to grow your financial well-being this year and for your family in years to come.

Sources:

https://www.irs.gov/taxtopics/tc409

https://www.schwab.com/learn/story/year-end-portfolio-checkup-5-tax-smart-tips

https://www.fidelity.com/learning-center/smart-money/401k-contribution-limits

https://www.schwab.com/learn/story/what-to-know-about-catch-up-contributions

https://www.dafgiving360.org/tax-law-changes

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-iras

https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-iras-distributions-withdrawals